You're helping your friend move apartments when they ask you to drive their truck to the new place. Twenty minutes later, you're sitting in an ambulance, wondering whose insurance will cover your medical bills.

The paramedic is asking about your pain level, but your mind is racing with different concerns entirely.

If you get into an accident with someone else's car, the questions start flooding in before you've even left the scene.

- Will you be stuck paying thousands in medical bills because you weren't driving your own vehicle?

- Should you call your insurance company first, or does the car owner's policy take priority?

- What happens if the friend or family member who owns the car starts pointing fingers, claiming you were driving recklessly or should never have been behind the wheel?

These concerns are completely natural when you get in an accident in someone else's car.

At Raphaelson & Levine, our car accident attorneys hear these exact worries from clients almost daily, and we understand why this situation feels so vulnerable.

You're already dealing with physical pain and the trauma of an accident, and now you're facing questions auto insurance policies that feel designed to confuse rather than help.

We've seen clients lose sleep over whether they'll be abandoned by both insurance companies, caught in a gap where the car owner's insurer says it's not their problem, and your own policy claims you weren't driving a covered vehicle.

When you're behind the wheel of someone else's car, the fear of being left financially responsible for an accident that wasn't even your fault can feel overwhelming.

Here's what we want you to know: You may have access to multiple sources of compensation that can fully cover your medical expenses, lost wages, pain and suffering, and more.

Over three decades, we've walked hundreds of clients involved in collisions while driving a work vehicle, rented vehicle, or a friend's borrowed car.

In this article, you'll learn how to protect your legal rights, access multiple sources of compensation you may not know exist, and maximize your car accident settlement after a crash in another person's vehicle.

.webp)

Understanding New York's Multiple Coverage Sources: Who Pays?

The good news is that when you're asking "whose insurance covers a borrowed car," the answer in New York is often "multiple policies." This typically means more compensation may be available for your injuries.

Primary Coverage: The Vehicle Owner's Insurance Policy

If you borrow a car, whose insurance covers it first? In most cases, the car owner's car insurance coverage provides primary protection for your injuries, even if you don't have a valid driver's license at the time of the car crash.

If the person driving was unlicensed, we'll review all policy terms and underwriting language to identify any explicit exclusions that may void or alter your coverage.

The car insurance company handling the vehicle involved must provide these benefits regardless of determining liability or the driver's fault.

This means you're entitled to immediate medical coverage and lost wage benefits up to the car owner's insurance policy limits, typically $50,000 per person in New York.

We've seen clients breathe a sigh of relief when they learn this.

You're not left hanging because you weren't driving your own vehicle. No-fault benefits kick in whether you caused the accident, another driver was at fault, or it was simply an unavoidable collision.

Secondary Coverage: Your Own Car Insurance Policy

Your own auto insurance company often provides secondary or excess coverage when you're driving someone else's car.

If the person's vehicle you borrowed doesn't have adequate coverage, your insurance provider may offer comprehensive coverage that applies even when you're driving with the owner's consent.

Your uninsured and underinsured motorist coverage can be particularly valuable.

If the car you borrowed doesn't have adequate coverage, or if an at-fault driver lacks sufficient insurance, your own policy may provide the additional protection you need.

Third-Party Coverage: At-Fault Driver's Insurance

When another driver causes the car crash while you're behind the wheel of a someone else's vehicle, their property damage liability coverage and bodily injury protection becomes a third source of potential compensation. Regardless of whether the accident exceeds the state minimum coverage requirements.

An experienced car accident lawyer at our firm will gather witness statements, medical records, and documentation (like driving record) to build a comprehensive case.

We recently helped a client recover maximum compensation when she was rear-ended while driving her sister's car. The sister's insurance provided $50,000 in PIP benefits, our client's own policy contributed another $100,000 in underinsured motorist coverage, and the at-fault driver's insurance paid $190,000 in liability damages.

Without understanding these multiple coverage sources, our client might have accepted far less compensation for her serious back injuries.

Understanding these coverage layers is just the beginning. Once you know the money is there, the next question becomes: how do you actually access it? That's where knowing your specific rights as an injured driver becomes crucial; because insurance companies won't volunteer this information.

Your Rights When Driving Someone Else's Vehicle

Many clients ask us, "If I'm driving someone else's vehicle and get hurt, do I have the same rights as if I were in my own car?" The answer is absolutely yes; and sometimes you may actually have more options for compensation.

You Have the Same Rights as Any Accident Victim

An accident driving someone else's car doesn't diminish your fundamental rights as an injury victim. You're entitled to immediate medical treatment without worrying about who's going to pay the bills initially.

Whether you're in the same household as the vehicle owner or a complete stranger who received permission to drive. When an accident occurs, your rights remain the same.

You have the right to pursue full compensation for all your injuries. If your injuries meet New York’s “serious injury” threshold, you have the right to also pursue pain and suffering damages. And you absolutely have the right to legal representation.

Insurance corporations can't pressure you to "handle this quietly" just because you were the person driving a borrowed vehicle.

Unfortunately, just knowing your rights often isn't enough.

Insurance companies are counting on your uncertainty about borrowed car accidents to minimize what they pay you. The tactics they use are predictable, and once you recognize them, they lose their power to intimidate.

Permission vs. Permissive Use

When you borrow a car with the owner's permission—whether that's explicit ("here, take my keys") or implied (you've borrowed it before with no objection)—you're covered under what's called "permissive use." This protection extends to borrowing from friends, family members, coworkers, or anyone else who gives you permission to drive their vehicle.

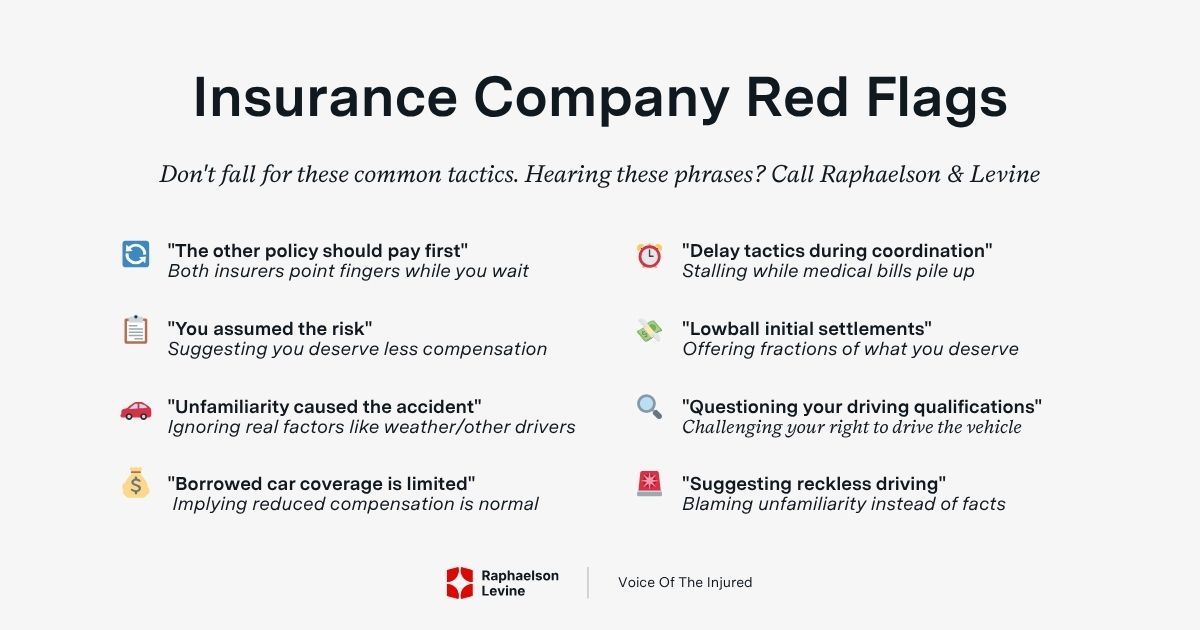

Common Insurance Company Tactics To Minimize Your Settlement

Insurance companies have perfected the art of minimizing payouts on borrowed car accidents. They're counting on your unfamiliarity with the system to work in their favor.

Our personal injury attorneys have seen these tactics hundreds of times, and know how to protect you from accepting far less than you deserve.

Common tactics we encounter:

- "The other policy should pay first" — The car owner's insurer points to your policy while your company claims the vehicle owner's coverage is primary. Both hope you'll get frustrated and accept whatever minimal offer one eventually makes

- "You assumed the risk by driving someone else's car" — They suggest you're somehow less entitled to compensation because you weren't in your familiar vehicle

- Claiming unfamiliarity caused the accident — Insurers argue the collision wouldn't have happened if you'd been driving your own car, ignoring factors like weather, other drivers, or mechanical failures

- "Borrowed car coverage is limited" — Some policies may have lower limits or step-down provisions for non-listed drivers, but implying that borrowing vehicles means accepting reduced compensation simply isn't true under New York law

- Delay tactics during multi-policy coordination — Complex situations create perfect opportunities to drag out settlements while mounting medical bills pressure you into inadequate offers

- Lowball initial settlements — We recently had a client receive a $15,000 offer for injuries that ultimately required $85,000 in medical treatment. The insurer claimed the borrowed car situation "complicated" the claim

- Questioning the person driving's qualifications — Insurance providers may challenge whether you had proper insurance information at the time of the car crash

- Suggesting reckless driving — They often argue the person driving was unfamiliar with the vehicle, or ignoring other factors

These arguments rarely hold up under scrutiny, but they can intimidate accident victims into accepting inadequate settlements. We've seen New Yorkers nearly lose tens of thousands of dollars because they didn't understand these were negotiating tactics rather than legal reality.

Fighting these tactics isn't just about principle, it's about ensuring you receive every dollar you're entitled to. The difference between accepting an insurance company's initial position and pursuing maximum compensation with an experienced car accident attorney can literally be life-changing.

Here's what's actually available to you under New York law.

Maximizing Your Personal Injury Settlement

When you're seriously injured while driving someone else's car, understanding the compensation you may be entitled to can mean the difference between full financial recovery and ongoing hardship. Here's what you may be entitled to in a car accident settlement in New York:

Economic Damages

- Current and future medical expenses: Not just your emergency room visit, but ongoing treatment, surgery, and rehabilitation that may continue for months or years after your accident

- Lost wages and diminished earning capacity: Compensation for missed work days and any reduction in your ability to earn income if your injuries affect your job performance or career prospects

- Rehabilitation and therapy costs: Physical therapy, occupational therapy, and psychological counseling often represent thousands of dollars in expenses that many clients don't initially consider.

Non-Economic Damages

- Pain and suffering compensation: Your physical discomfort and emotional distress deserve recognition beyond just covering medical bills—these damages acknowledge the daily struggle of living with injury-related limitations.

- Loss of enjoyment of life: We've helped clients recover damages for missing their child's baseball season due to back injuries or being unable to garden after hand trauma. Injuries that steal life's simple pleasures deserve compensation.

- Emotional distress and mental anguish: The psychological impact of serious accidents often requires professional counseling and can affect your relationships, sleep, and overall quality of life

Why Multiple Policies Can Mean Higher Recovery

- Stacked coverage limits may increase total compensation: Instead of being limited to one policy's collision coverage limits, you may have rights to more compensation by combining multiple sources, depending on the circumstances, everyone involved, and policy terms.

This is particularly important when an accident exceeds the state minimum coverage requirements, and can help offset potential insurance premiums increases. - Secondary insurance fills coverage gaps: When the primary policy reaches its limits, your own uninsured/underinsured motorist coverage can continue funding your recovery without interruption.

We recently helped a client recover over $495,000 by coordinating three different insurance policies after he was injured in his coworker's vehicle. Without understanding these layered coverage options, he might have accepted the initial $50,000 offer and struggled with ongoing medical expenses for years.

Of course, pursuing maximum compensation becomes more complicated when friendship enters the picture. The guilt some clients feel about 'going after' their friend's insurance can be overwhelming. Unfortunately, this emotional response often costs them the money they need to rebuild their lives.

What Happens If You Have an Accident While Driving Your Friend's Car?

What happens if you have an accident while driving your friend's car?

The answer depends largely on how you handle the immediate aftermath, and whether you let friendship complicate what should be straightforward insurance and legal decisions.

Immediate Steps to Protect Your Rights

Your health comes first, always.

- Seek medical attention even if you feel "fine," adrenaline can mask serious bodily injuries. Having immediate medical documentation protects your claim later.

- If you're able, document the accident scene with photos and gather insurance information from all parties from witnesses.

- Don't admit fault to anyone at the scene, and never give recorded statements to insurance adjusters without speaking to an attorney first.

How Friendships Can Complicate Insurance Claims

Here's where things get emotionally complicated. Your friend might pressure you to "handle this between us" or avoid involving insurance to protect their rates. We understand the instinct to preserve relationships, but we've seen too many cases where someone suffered permanent injuries but didn't pursue compensation to "keep the peace."

Don't let loyalty cost you your future. Proper insurance handling actually protects both of you. Your friend's rates may increase whether or not you file a claim, but failing to document injuries properly can leave you facing thousands in medical bills with no recourse later.

We recently worked with a client who waited months to contact us because she didn't want to "hurt" her sister's insurance situation.

By then, her untreated back injury had worsened significantly, requiring surgery that could have been prevented with immediate proper care. The delay also complicated her insurance claim. Insurance companies become suspicious when there's a gap between accident and treatment.

These emotional complexities are exactly why certain car accident cases involving someone else's car demand professional legal guidance. When relationships, multiple insurance policies, and serious injuries collide, the situation becomes too complex (and too important) to handle alone.

When You Need A Car Accident Lawyer

While some borrowed car accidents can be handled directly with insurance companies, certain situations demand professional legal representation. Specific circumstances almost always require attorney involvement, and waiting too long to seek help often makes recovery more difficult.

- Serious Injury Cases: When your injuries are severe and involve multiple insurance providers, an experienced car accident attorney becomes essential. Property damage disputes and complex coverage coordination require professional legal guidance.

Permanent disabilities that affect your ability to work, care for your family, or enjoy activities you once loved require comprehensive legal strategy. - Disputed Coverage Cases: Insurance companies sometimes deny coverage entirely for borrowed car accidents. They might claim you didn't have permission to drive the vehicle, that the policy excludes certain types of drivers, or that coverage limits don't apply to your situation.

These disputes often involve complex policy language that even experienced adjusters interpret differently.

Recognizing you need an attorney and finding the right one are two different challenges.

When you're dealing with injuries, insurance confusion, and relationship stress, the last thing you need is uncertainty about your legal representation.

That's where our three decades of handling these exact cases becomes your advantage.

Why Choose Raphaelson & Levine Law Firm

At Raphaelson & Levine, we've been guiding New York families through these exact situations for over three decades.

We've recovered more than $1 billion for clients since 1992, and up to 25-times more compensation than our client's were initially offered.

Many of our cases involving the complex insurance coordination that borrowed car accidents require.

Our legal expertise has earned recognition among "Best Car Accident Lawyers in New York City" by Expertise.com, but what we're most proud of is how we remove the burden from your shoulders.

When multiple insurance companies are pointing fingers at each other, we step in and force them to fulfill their obligations. You shouldn't have to become an insurance expert while recovering from injuries.

We handle all the coordination between the car owner's coverage, your own insurance, and any third-party liability claims.

Our clients often tell us they had no idea how complicated these cases could become until we started uncovering additional sources of compensation they never knew existed.

During our initial conversation, we'll evaluate your case, explain your options clearly, and help you understand what to expect moving forward.

The consultation is free, and you don't pay unless we recover compensation for your injuries.

Located across from Penn Station in Midtown Manhattan, we're here when you need us most.

Call us today at 212-268-3222, or contact us online.